We all know that the Indian stock market has been dominated by two most prominent players - the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE). But come 2026, and a third player is out to compete these two giants, and you heard it right, it is the Metropolitan Stock Exchange of India (MSEI), formerly known as MCX-SX.

Backed by major retail brokers like Groww and Zerodha, and armed with fresh capital and innovative incentives, MSEI is all set to become another big player in the stock exchange market.

This blog is all about why MSEI was created, its full history, strategy, current performance, and what it really means for investors and traders.

NSE-BSE Duopoly: Why India Needed a Third Exchange

Before MSEI, trading was heavily concentrated on NSE and a little to BSE. See the table below:

Product Edge: Plans for Friday index F&O expiries (complementing NSE’s Tuesday and BSE’s Thursday under SEBI’s two-weekly-expiry rule)

Listing Fees: Zero or heavily discounted fees, especially for SMEs

Revenue: Transaction, membership, and listing fees, but heavily subsidised in the early phase

Product Offerings by MSEI

MSEI is a near-full-service exchange with:

Equity (cash) as stocks, ETFs, REITs, InvITs

Equity Derivatives (Futures & Options)

Currency Derivatives (USDINR, EURINR, etc.)

Interest-Rate Derivatives & Wholesale Debt

SME Platform

(Notably, no commodity derivatives - those remain with MCX/NCDEX.)

Current Performance: The Numbers Tell a Tough Story

Despite the hype and capital infusion, you should check these numbers, as they are telling another story:

Daily equity volume (early Feb 2026): ~₹0.5 million (vs NSE’s average ₹1.12 lakh crore)

Market share: ~0% in both cash and F&O

FY2022-23: Only 3.8% of MSEI-listed securities saw any trading (vs 78% on BSE)

Order-book depth: Only ~12 actively traded stocks post-relaunch

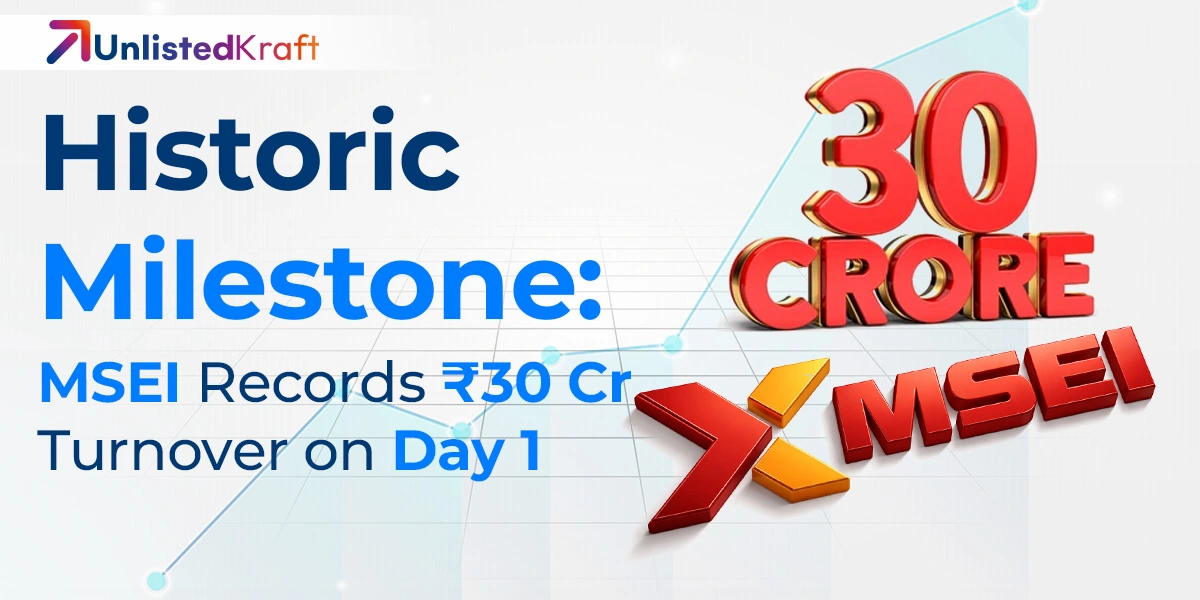

NSE and BSE have responded aggressively in the past (e.g., zero fees on currency futures to counter MCX-SX) and continue to enjoy massive scale advantages. Also, on April 1, 2026, MSEI showed a record-breaking opening performance. Its newly launched Market Maker Programme in the equity segment generated ₹30.36 crore in turnover on Day 1 alone, with 7,80,674 shares traded by 3:30 PM IST.

Investor Benefits vs Risks

Now, let us see what the benefits are for investors and also weigh in the risks involved:

Potential Benefits

Zero transaction fees during the subsidy period

Access to new Friday experiences and niche products

Potentially lower long-term costs if competition intensifies

Additional venue for better price discovery in select stocks

Key Risks

Extremely thin liquidity, which indicates wider spreads and execution risks

Subsidy expiry after June 2026

Regulatory risk if volumes remain below SEBI’s ₹1,000 cr threshold

Order-flow fragmentation across three exchanges

Recommendations for Investors & Traders

The following are some of the important recommendations for investors as well as for traders:

Use MSEI selectively: Only for incentive-covered stocks or new expiry opportunities

Keep order sizes modest

Prefer highly liquid names with active market-makers

Monitor real-time volumes, bid-ask spreads, and depth

Treat MSEI as an experimental venue, not a core platform, until it proves sustained traction

Summary

MSEI’s revival is a bold and much-needed attempt to inject competition into India’s equity markets. With strong backers, fresh capital, and smart incentives, it has a fighting chance to create a viable third alternative.

However, breaking a 25-year-old duopoly is an uphill battle. Success will depend on whether MSEI can convert short-term subsidies into genuine, sticky liquidity and long-term order flow.

If MSEI can maintain momentum beyond June, it could become a meaningful game-changer for Indian investors. If not, it risks remaining a niche player. For additional reading and information, you can read our detailed company analysis on MSEI

Frequently Asked Questions

Q1: Are MCX and MSEI the same?

No. MCX (Multi-Commodity Exchange) is India’s leading commodity derivatives exchange. MSEI was originally promoted by MCX as MCX-SX (MCX Stock Exchange) in 2008. It was later rebranded as the independent Metropolitan Stock Exchange of India (MSEI) in 2014. They are separate entities.

Q2: Who owns the Metropolitan Stock Exchange?

MSEI is owned by a group of shareholders led by major retail brokers. In 2024-25, Groww (Billionbrains) and Zerodha (Rainmatter), along with other fintech investors, infused ₹1,240 crore. Earlier investors included Peak XV (Sequoia), Rakesh Jhunjhunwala, Radhakishan Damani and institutional funds. It remains an unlisted company.

It does not offer commodity derivatives (those remain with MCX/NCDEX).

Q4: Is MSEI a good buy?

For unlisted shares: High-risk, high-reward. It has strong backers and fresh capital, but volumes are still negligible, and profitability is uncertain. Suitable only for aggressive, long-term investors who can tolerate illiquidity.

For trading: Not yet recommended as a core platform. Use it selectively for fee-waived trades or Friday expiries while liquidity is thin. Treat it as experimental until volumes improve significantly.

Q5: Why was MSEI created when NSE and BSE already existed?

SEBI wanted to break the NSE-BSE duopoly (90-92% + 8-10% market share) to increase competition, reduce trading costs, encourage innovation, and improve market resilience.

Q6: What is MSEI’s current market share and volume?

Extremely low (~0%). Post-relaunch in Feb 2026, daily equity volume is around ₹0.5 million compared to NSE’s ₹1.12 lakh crore daily average. Liquidity is still very thin.

Q7: What is MSEI’s main strategy to attract traders?

Heavy liquidity subsidies (transaction fee waivers + ₹40 lakh/month incentives to market-makers) till June 2026

Friday index F&O expiries (new product under SEBI rules)

Modern tech platform (GMEX partnership)

Zero/low listing fees, especially for SMEs

Backing from brokers controlling ~40% of retail demat accounts

Q8: What are the biggest risks of trading or investing in MSEI?

Very low liquidity, meaning wide spreads and execution risk

Subsidies end in June 2026 (volumes may drop)

Regulatory risk: SEBI can de-recognise the exchange if annual volume stays below ₹1,000 crore

Order-flow fragmentation across three exchanges

Q9: When did MSEI relaunch trading?

February 1, 2026 (Union Budget Day), with a dedicated Liquidity Enhancement Scheme running from January to June 2026.

Q10: Will MSEI succeed in challenging NSE and BSE?

Too early to say. It has strong financial backing and smart incentives, but breaking a 25-year duopoly is extremely difficult. Success depends on whether it can convert temporary subsidies into sustainable order flow and liquidity after June 2026.

Author: Diwakar Singh

Diwakar Kumar Singh is a BFSI specialist and finance writer with over 7 years of hands-on experience in financial research, content creation, and analysis.

A Gold Medalist in MBA (Marketing) from IMT, he combines deep analytical skills with practical insights gained from evaluating companies, IPOs, unlisted shares, financial ratios, and investment opportunities. Diwakar has personally analysed hundreds of financial instruments and market scenarios, which he uses to break down complex topics into clear, actionable advice.

He has authored numerous in-depth finance articles, published multiple books internationally, and contributed to research publications. His work focuses on helping everyday investors and readers make better-informed financial decisions through well-researched, evidence-based explanations that are always grounded in real-world application rather than theory alone.